As we head into the final quarter of 2023, the industry is in much better shape than at the start of the year. Looking back to my forecast for the year ahead in January, I was realistic about the market pressures, while highlighting opportunities for those companies looking to diversify.

Today, many of those squeezes on household finances that I detailed, are now starting to ease. For example, inflation continues to fall. It may still be at 6.7%, above the target of 2%, but it was above 11% a year ago. This downward trajectory reassured the Bank of England enough for them to keep the interest rate at 5.25% in September, and they expect inflation to fall to around 5% by the end of the year.

This is good news for homeowners who are seeing that confidence filter down to reduced high street mortgage interest rates. And as the cost of borrowing starts to come down, homeowners – as well as businesses – should look to increase investment.

The biggest impact on inflation was the war in Ukraine and the spiralling energy costs. While the war continues, energy costs have come down and seemingly stabilised. The energy regulator Ofgem subsequently reduced the energy cap for the final quarter of 2023, bringing the average dual-fuel bill down to below £2,000 for the first time since April 2022. Energy shortage also seems unlikely this winter.

We are seeing this steady return to confidence play out in the Business Pilot Barometer, as we have done for the last couple of months.

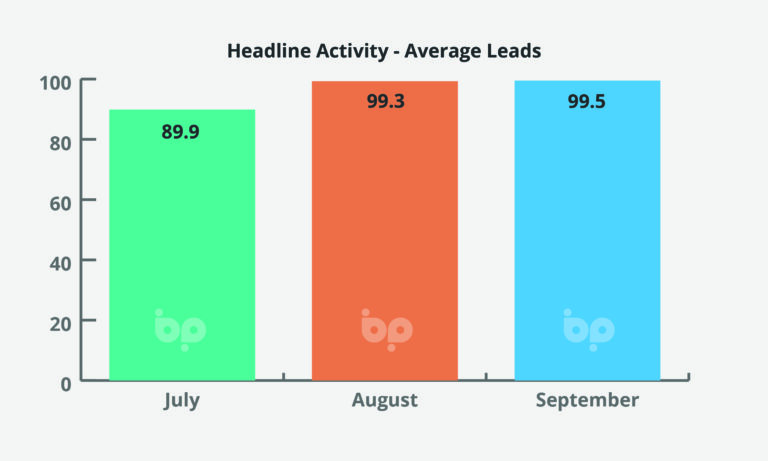

The headline figure is that the average number of leads remains strong. While September was marginally up on August at 99.5, it was 27.2% higher than the same period last year. I think this is remarkable because this final quarter will lay the foundations for how we expect 2024 to look in January, and this is a good start.

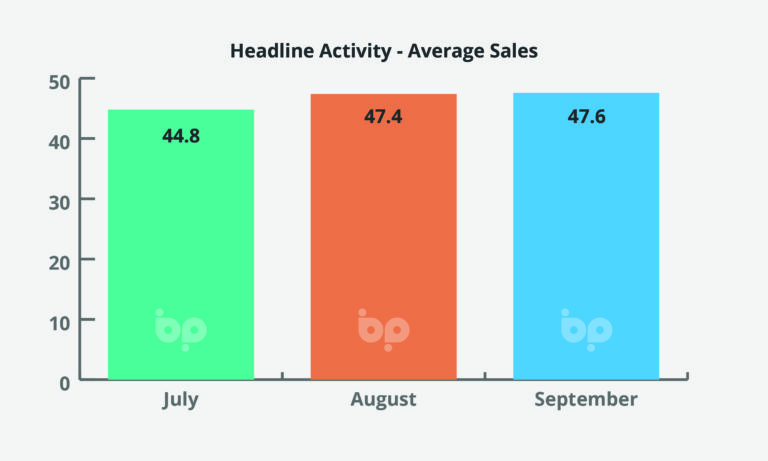

September’s average sales figures follow a similar pattern: at 47.6, September was marginally up on August, but 29.3% up on the same period last year. Together, these demonstrates that industry is in a more positive place that it was heading into the difficult winter of 2022.

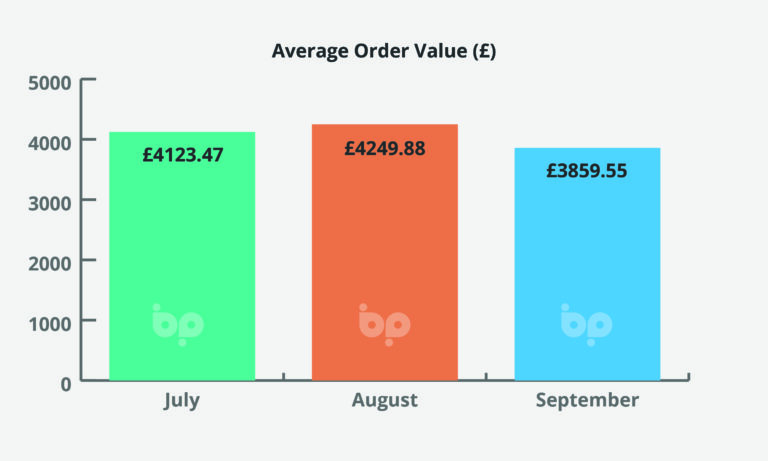

One figure that caught me slightly off guard was the average order value. I had been expecting to see this figure increase as we head towards the end of the year, as in previous years. But, at £3,860, it is down 10.1% on August, and 20.4% on September 2022.

On closer analysis, this is reflecting the positive shift in behaviour we detailed above. For most of 2023, the market for new windows and doors has relied heavily on the upper end of the market, and homeowners who have spare cash to invest in home improvements, thus pushing up that average order value.

Instead, we are seeing increased interest from the rest of the market. I don’t think this means you should ditch the coloured flush casements, but rather give equal billing to your standard products when it comes to marketing.

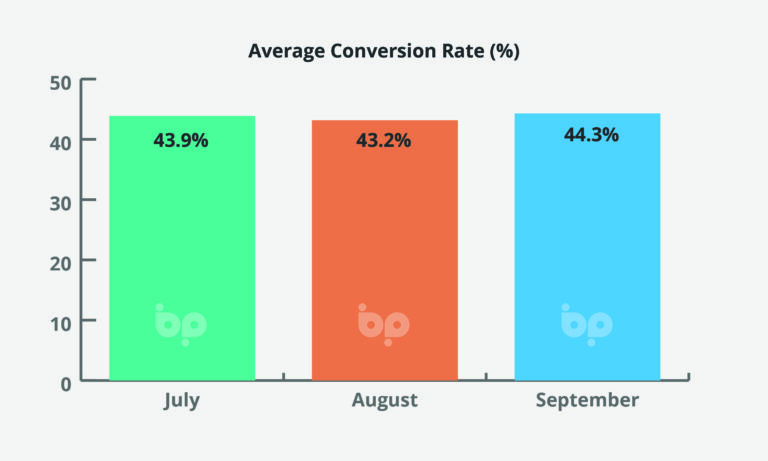

Finally, we continue to see the average conversion rate continue to rise. This time last year, it stood at 34.8%. In September 2023, that figure was 44.3%, which is approaching the territory of companies converting one in every two leads.

I’ve argued that this may be down to the fact that homeowners are conducting more research before approaching fewer window companies for quotes, but don’t forget that these figures are taken from companies that use the Business Pilot software to help manage leads, quotes and conversions. So, if you are not a Business Pilot customer, and your conversion rate is below 44.3%, maybe now is the time to look systemising your processes?