…offers a monthly analysis of the key trends defining window and door retail. It draws on real industry data collated by Business Pilot, the cloud-based business management tool developed by installers for installers.

Neil Cooper-Smith, Senior Analyst, Business Pilot:

The reaction of markets (and the UK national media) to emergence of Omicron, the new variant of COVID-19, echoes what we’ve seen every time cases of COVID-19 have risen, or we’ve entered a new period of lockdown.

Oil prices have dropped in the expectation that UK and global travellers will be grounded – or at least travel in fewer numbers – shares in airlines and hospitality sectors have also fallen, and the media is full of stories about an impending collapse in consumer confidence.

What has that meant for the window and door industry on each of those occasions previously? We’ve seen resurgent demand and exponential growth.

This time may, however, be a little different, less because of the impact of Omicron on consumer confidence – it sounds perverse to say it, but COVID has been good for business, at least the sales side. When people can’t spend on holidays and dining out, they spend on ‘stuff’ including home improvements.

That is if inflation isn’t increasing the cost of living, which it is.

The Centre for Economics and Business Research (CEBR) has projected that inflation will hit 4.6% (up from the current 4.2%) by Christmas. That would mean average household costs could rise by as much as £1,700 per year.

This would mean this time around rather than UK households sitting on furlough and home working windfalls as they did through much of the last and preceding year, households will feel the pinch.

This is at a time when inflationary costs within the window and door supply chain, are likely to push up the cost of purchase to the homeowner (and those within the supply chain), further.

Energy price increases are hitting homeowners and business, but companies face additional pressures not least wage inflation.

According to figures published by the Office for National Statistics last month, average wages increased by 5.8% July to September and are likely to increase further running into the end of the year.

Raw materials also continue to rise. PVC resin supply is precarious, with capacity across Europe down to 70% and prices rising to as high as $2,500 per tonne last month, even before energy surcharges kick in. Supply chains from the Far East also remain disrupted making further product price inflation likely.

In short, the price point installers are going to have to charge to the homeowner are going to need to rise going into 2022, at the same time as homeowner’s feel the bite of wider inflation.

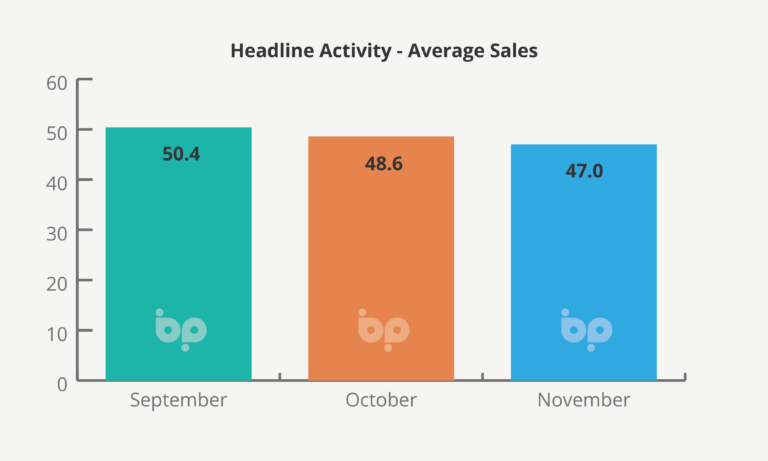

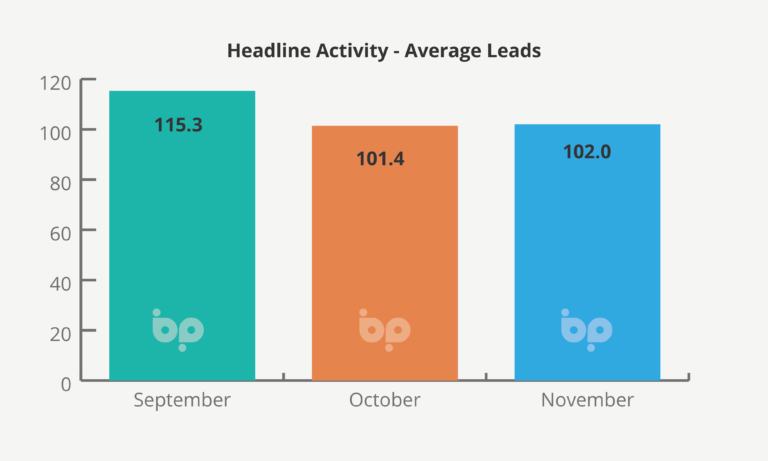

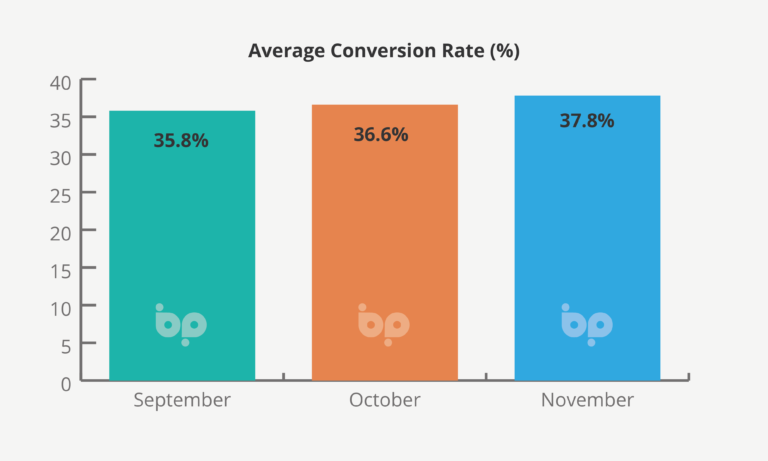

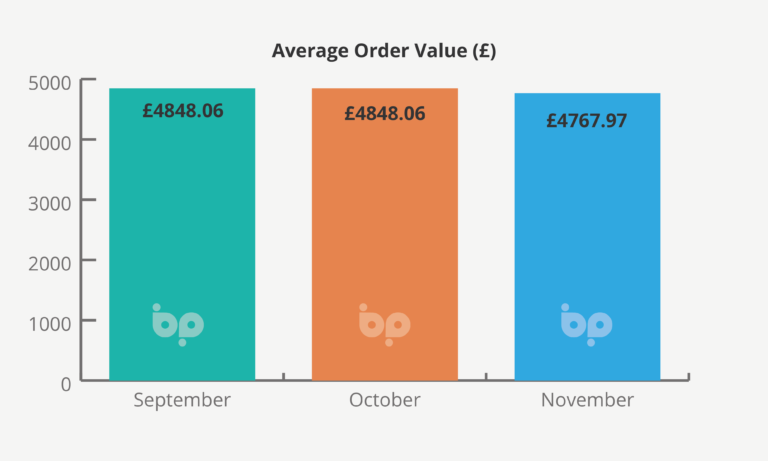

According to our data, sales of windows and doors were down slightly (3%) last month [NOV] on October the third successive drop; leads were moderately up; and the conversion rates also rose to 37.8% from 36.6%.

Some of this can be attributed to the run into Christmas, pre-existing disruption to the supply chain and that installers haven’t necessarily been driving lead generation.

But it is a hint that inflation may be making homeowners more cautious – and on that basis – may be less easily parted with their cash as we head into the new year.

Business Pilot is a powerful CRM, which mobilises the power of cloud-based technologies, to give installers complete visibility of each and every element of their operation from leads and conversions to job scheduling, cost of installation, service calls, and financial reporting.

Accessible across all devices, from desktop to phone, it supports installers in running their businesses more profitably.