…offers a monthly analysis of the key trends defining window and door retail. It draws on real industry data collated by Business Pilot, the cloud-based business management tool developed by installers for installers.

Neil Cooper-Smith, Senior Analyst, Business Pilot:

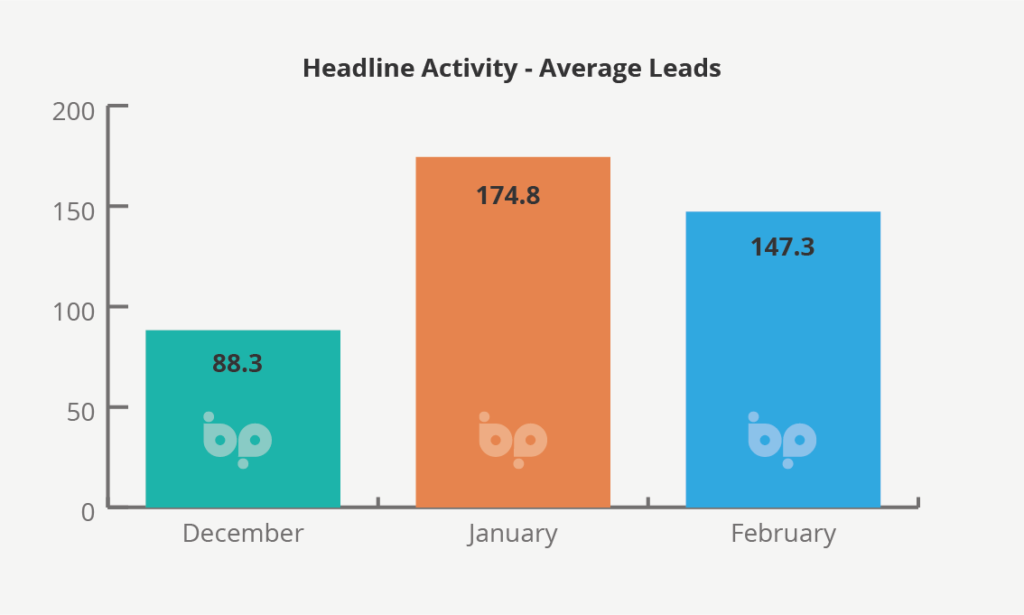

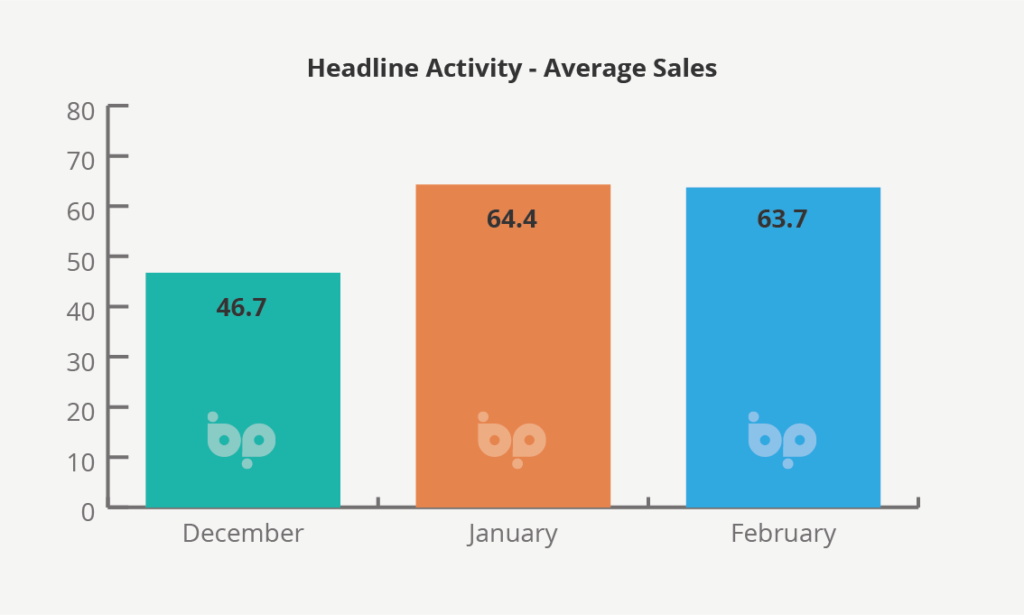

The industry saw a significant uplift in January, with the number of leads jumping by 97% on figures for December. Although some of this may be attributed to lower levels of activity in retail in December and in the holiday period, it nonetheless represents a significant spike in activity.

This is consistent with a wider analysis which reported increased levels of consumer confidence with the general election result and increased clarity on Brexit

The consumer confidence index from market research firm GfK rose for the third month in a row, hitting a score of minus seven in February. This compared to a reading of minus 13 a year earlier.

GfK attributing this to a February backdrop of rising wages and house prices, low unemployment and stable inflation.

COVID-19, however, in common with other sectors continues to hang menacingly over the industry, with leads tailing-off towards the end of last month [Feb] contributing to a month-on-month fall on January of 16%.

With the virus and its impact expected to get worse before it gets better, it could be expected to suppress consumer demand in the short-term.

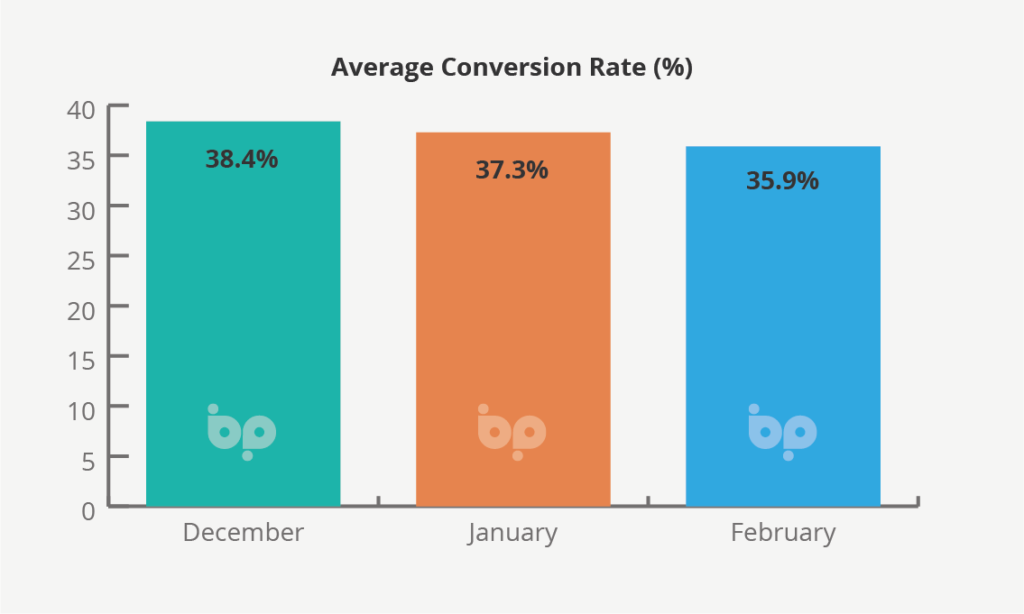

Average conversion rates, however, remained high across the three-month period including 38.4% in December. This remained high in January despite the spike in new leads at 37.3%, tailing off marginally in February to 35.9%.

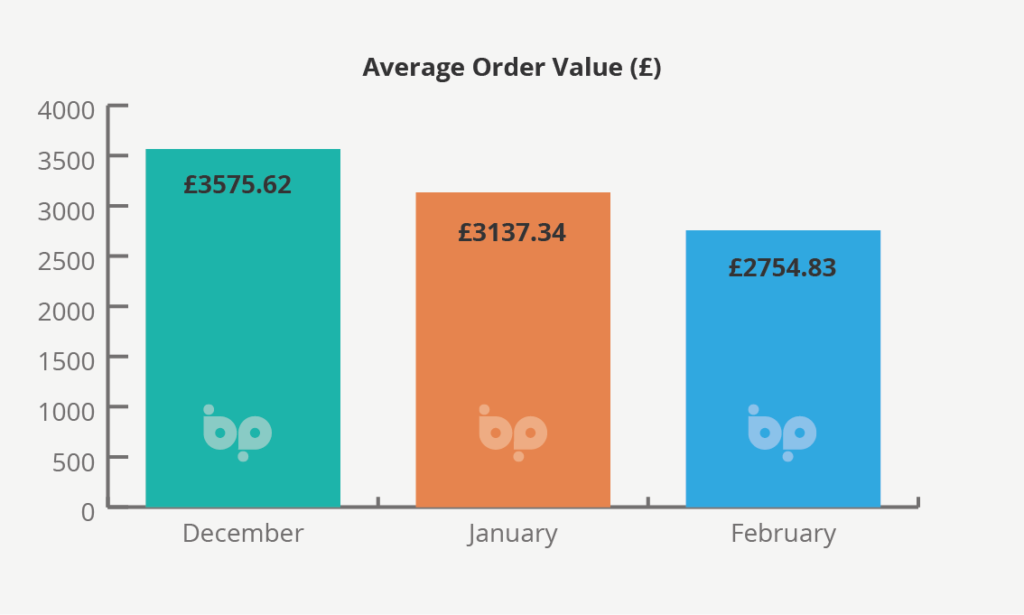

This headline figure, however, hides a 31% drop in sales of timber products January to February and 12% in aluminium. Sales of PVC-U products remained comparatively constant. This drop in sales of higher value products contributing to a 12% drop in average order values in the last month to £2,755.

Business Pilot is a powerful CRM, which mobilises the power of cloud-based technologies, to give installers complete visibility of each and every element of their operation from leads and conversions to job scheduling, cost of installation, service calls, and financial reporting.

Accessible across all devices, from desktop to phone, it supports installers in running their businesses more profitably.