March’s data paints a picture of a market that is continuing to stabilise – and, in some areas, strengthen, – against all odds, in an increasingly complex and uncertain economic backdrop.

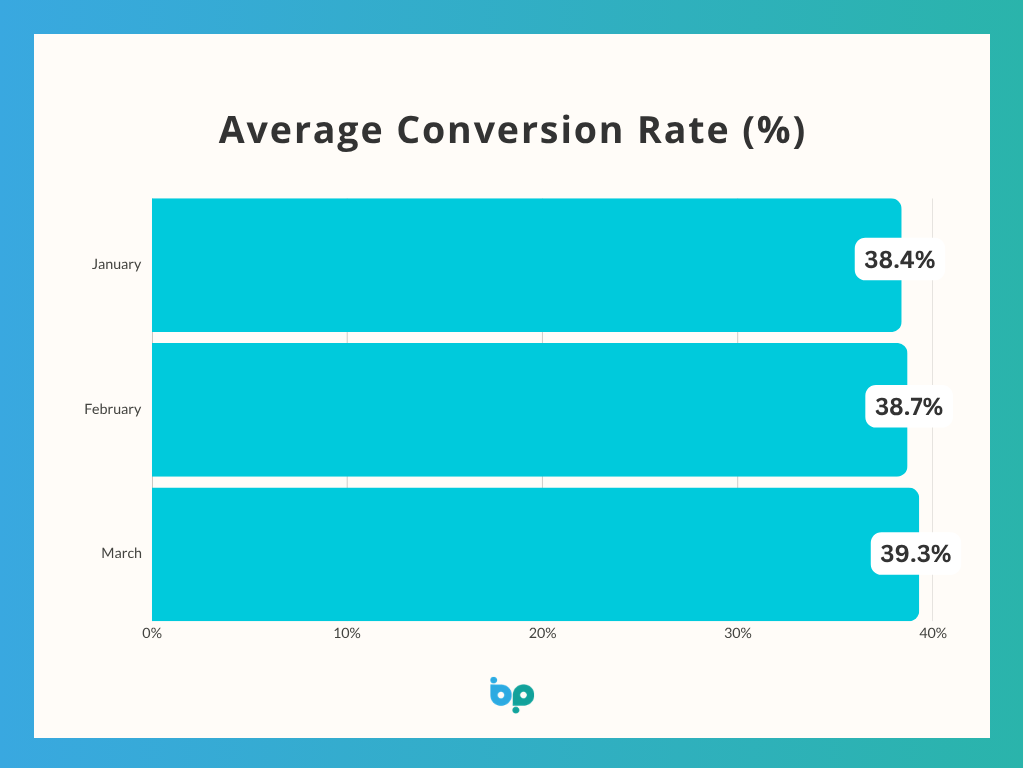

Conversion rates edged up again, rising from 38.7% in February to 39.3% in March – a modest but meaningful improvement of around 1.5%. This continues the gradual upward trend seen since the start of the year and suggests that, despite external pressures, installers are becoming more effective at turning opportunities into confirmed work.

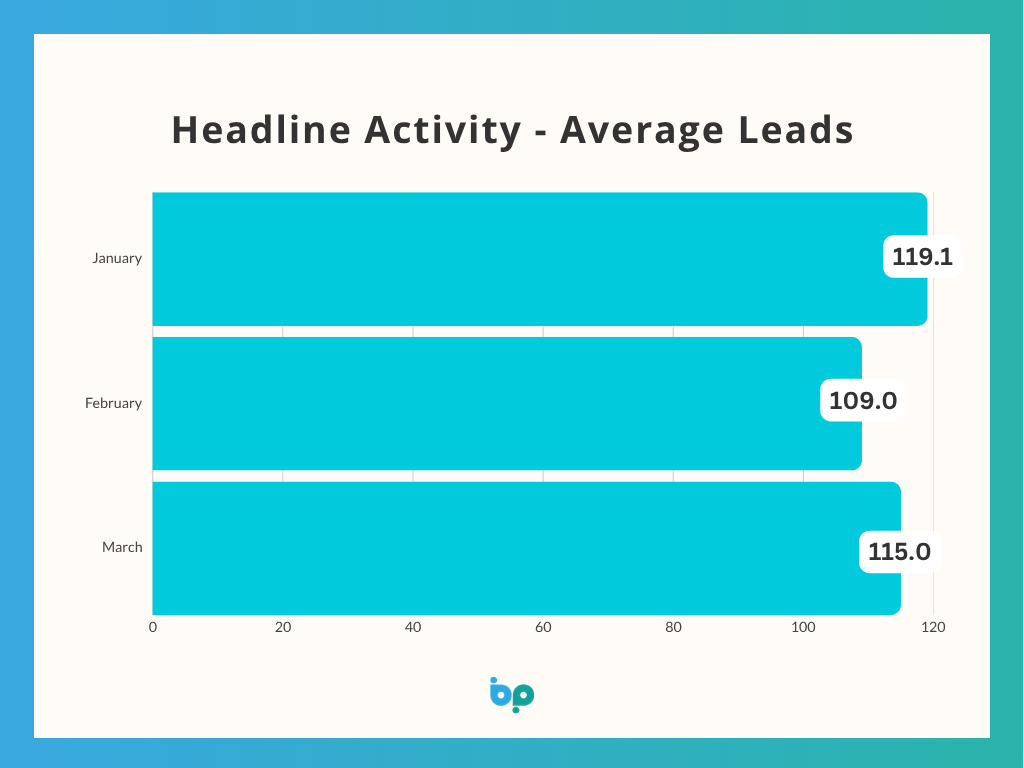

This is backed up by lead volumes; after February’s dip, March saw a partial recovery, with volumes increasing by around 5.5% month-on-month. While not a full return to January’s peak, this rebound suggests that underlying demand is still present, albeit more volatile.

Sales performances were also notably stronger in March, increasing by 7% compared to February, and continuing the positive momentum established at the start of the year. This means sales growth once again outpaced lead growth: an important signal that businesses are extracting more value from each enquiry.

In practical terms, this points to improved sales processes, stronger follow-up, and potentially better-qualified leads entering the funnel.

However, average order values fell by £817 to £3,876, from February’s unusually high peak. While this 17% decline may initially appear concerning, we believe that this is more accurately understood as a normalisation following a spike, rather than a collapse in demand. The February uplift likely reflected a concentration of higher-value projects, whereas March shows a broader mix of mid-range jobs returning to the market.

What makes this data particularly interesting is how these trends co-exist with wider economic factors.

UK inflation held at 3.0% in the year to February, but economists are now warning that rising energy costs linked to the conflict in Iran could push inflation higher again in the coming months. Indeed, oil prices have already surged sharply, driving up fuel costs and increasing pressure on both households and businesses.

This is already feeding into consumer sentiment.

Confidence slipped in March, with sentiment indicators falling further into negative territory, reflecting growing concern about personal finances and the wider economy. Consumer confidence indexes suggest a majority of UK consumers now expect the economic situation to worsen in the near term, driven largely by rising living costs and uncertainty linked to global events.

For the home improvement sector, this creates a nuanced environment. On one hand, rising costs – particularly energy, materials and interest rates – are likely to keep pressure on pricing and margins. On the other, the data suggests that when consumers do engage, they are increasingly decisive, with sales conversion and overall sales values holding up well.

Therefore, the key takeaway from March is that performance is being driven less by sheer volume and more by efficiency, process and positioning. In a market where demand is uneven and confidence is fragile, the businesses that continue to perform are those that can convert effectively, respond quickly, and maximise the value of every opportunity.

As external pressures, from geopolitical instability to rising costs, continue to shape consumer behaviour, the ability to manage pipelines, track performance, and refine sales processes becomes even more critical.

Tools like Business Pilot will be installer’s greatest ally, enabling them to respond to changing market conditions in real time, improve conversion, and maintain growth – even when wider economic signals remain uncertain.