April’s data paints a picture of a market that is continuing to adjust to a more uncertain and uneven trading environment, with performance increasingly shaped by efficiency rather than sustained growth in demand.

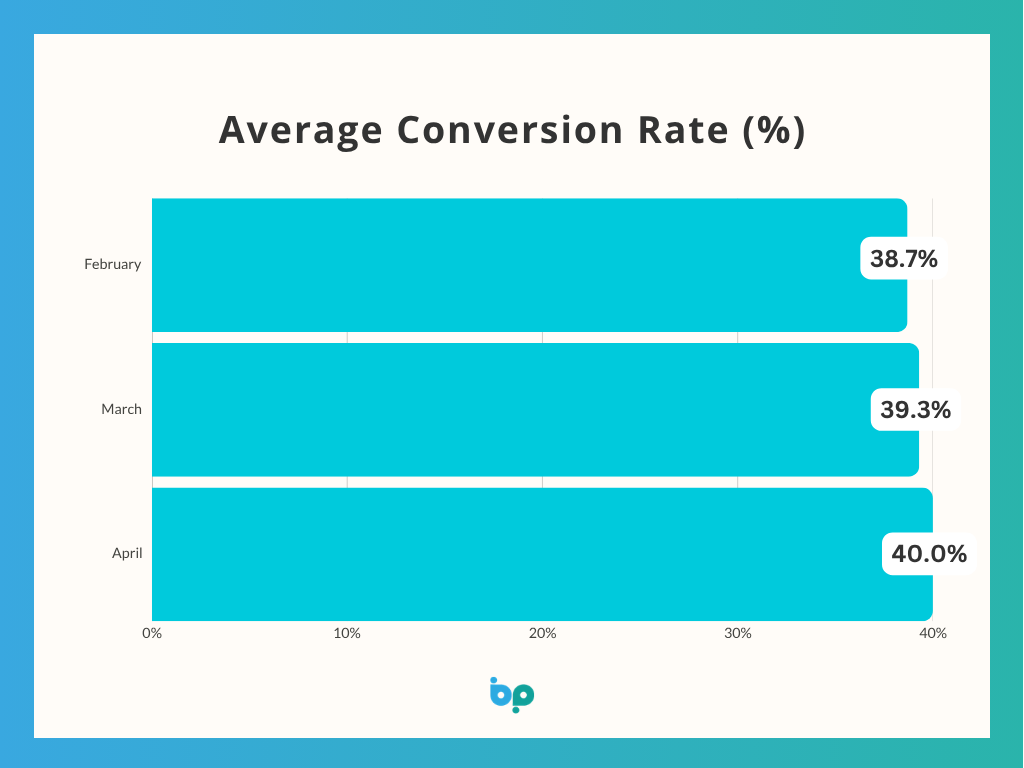

Conversion rates edged up again, rising from 39.3% in March to 40.0% in April, building on February’s 38.7%. This steady upward movement continues the trend seen since the start of the year and suggests that installers are becoming progressively more effective at converting opportunities into confirmed work.

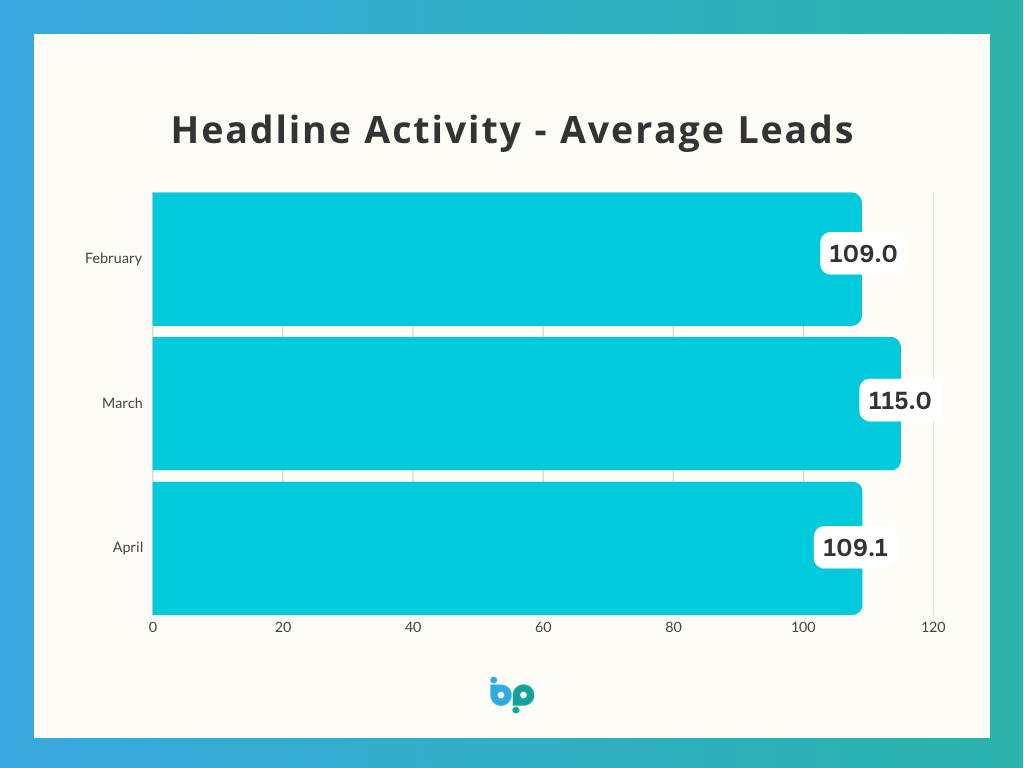

Lead volumes, however, remain more volatile. After increasing to 115 in March, average leads fell back to 109.1 in April, broadly in line with February’s 109.0. While this suggests that underlying demand remains present, it also highlights a lack of consistent momentum, with enquiry levels fluctuating from month to month.

Sales performance reflects a similar pattern. Having risen from 51.1 in February to 54.7 in March, average sales eased back to 50.6 in April. Importantly, this does not indicate a sharp slowdown, but rather a continuation of the more variable trading conditions seen in recent months.

What stands out is that, despite these fluctuations in both leads and sales, conversion rates have continued to improve. This indicates that businesses are extracting more value from each enquiry, supported by stronger sales processes, more effective follow-up, and potentially better-qualified leads entering the pipeline.

Lead times provide further insight into how the market is evolving. After remaining relatively stable at 26.6 days in February and 26.4 days in March, average lead times fell significantly to 21.8 days in April. This reduction suggests increased operational efficiency, improved capacity, or a softening of order backlogs, allowing installers to respond more quickly to demand.

Meanwhile, average order values appear to be stabilising following February’s peak of £4,693. Values fell to £3,876 in March before recovering slightly to £3,954 in April. In context, this points to a more balanced mix of project types, rather than a sustained shift towards either high- or lower-value work.

This remains closely linked to the wider economic backdrop. While inflation has stabilised in recent months, ongoing pressure from energy costs and global instability continues to weigh on household finances. Consumer confidence also remains fragile, with many households cautious about discretionary spending.

Taken together, April’s data reinforces a key trend seen throughout the year so far: performance is being driven less by growth in demand and more by how effectively businesses manage and convert the opportunities they receive.

For the home improvement sector, this creates a more selective market environment. Demand has not disappeared, but it is less consistent, and customers are more considered in their decision-making.

In practical terms, this places greater emphasis on process, responsiveness, and visibility. Businesses that can track performance closely, follow up quickly, and maximise conversion are best positioned to maintain output, even when enquiry volumes fluctuate.

Tools like Business Pilot play an increasingly important role in supporting this approach, giving installers the data and insight needed to manage pipelines effectively, improve conversion rates, and respond in real time to changing market conditions.